Written by: Lei Qiu

Low interest rates and massive stimulus-fueled debt raise investor concerns about potential long-term fallout. But when the cost of capital is this low, it revs up funding for innovation that ultimately fills the pipeline with robust opportunities, especially in technology.

Many investors are concerned what near-zero interest rates and the global economic fallout that aggressive stimulus measures may bring. Some concerns are understandable. But in fact, we see a silver lining in the lower cost of capital created by this environment. First, it helps generate ample, low-cost funding for innovative businesses and auspicious startups. Moreover, it can reward companies that proactively invest in research and development (R&D) to expand their growth opportunities.

Today’s low rates favor future growth initiatives, like R&D and venture capital (VC), especially in the innovation-charged technology sector. Beyond technology, areas like retail, healthcare, and even industrials and materials are also benefiting from innovation. As technological innovation continues to lower entry barriers, we have seen companies investing more heavily in forward-looking initiatives that can fuel growth as well as fortify their competitive moat.

Venture Capital and R&D Are Flashing Green

Equity investors with an innovation focus have been rewarded this year. There are many examples of how the pandemic accelerated innovation themes that were already on a success path before the crisis (digital migration and fintech come to mind). But the pandemic also worked to spotlight innovative startups with long-term potential.

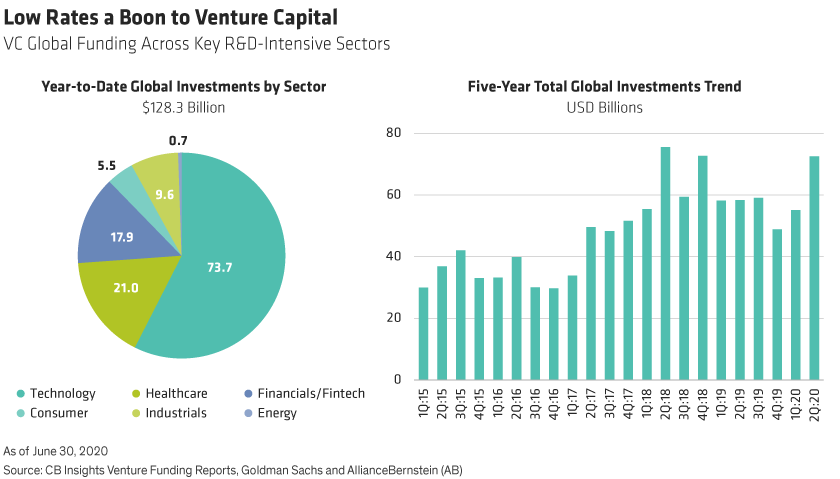

With the cost of capital support so historically low, VC providers are more than eager to invest in promising enterprises. And in technology, healthcare and other R&D-intensive sectors, global VC flows are approaching record highs (Display). This helps provide a bigger and promising pipeline of potential future winners for investors in publicly traded companies.

The low-rate environment also supports R&D investing—a bare necessity for any technology leader committed to staying relevant. Making smart investments helps enhance their outlook, generates opportunities and adds tangible long-term value, especially in investors’ minds.

In fact, companies that invest in R&D are being rewarded by the market, much more than those that resort to financial engineering, according to our research. We sampled 1,500 global companies across technology, healthcare, capital goods, autos and materials and consumer-discretionary sectors. Results showed R&D intensity, as measured by R&D/Sales, to be a significant positive contributor to future stock price performance. This especially bodes well for technology’s outlook, because more tech leaders are rightfully spending on R&D to stay ahead of consumer needs and other market forces that can shift on a dime.

Mergers and Acquisitions: Another Pathway to Innovation

Access to low-cost capital is also sparking more mergers and acquisitions (M&A). Highly valued companies are using their stock currency to bolster their product portfolios. And rather than look for M&As centered on incremental revenue or profit in the near term, investors are—and should be—focused on the types of transformational acquisitions with long-term strategic value in mind.

Technology innovators are particularly focused on M&A right now. For example, landmark deals were recently struck between chipmakers NVIDIA and SoftBank’s Arm; AMD and Xilinx in the processor space; and Marvell and Inphi, both niche semiconductor powerhouses. All are important players in the datacenter ecosystem, and the moves will bolster their end-to-end positioning in the new data center paradigm.

Some critics shun such aggressive M&A initiatives. These deals may seem akin to high-multiple stocks just buying higher multiples to shore up market-favorable financials. However, when determining which deals are strategically sound, investors should focus on companies with visionary leaders. Such companies take advantage of lower rates and higher multiples to pursue takeovers designed to augment their own offerings and sharpen a competitive edge. Investors seem to have endorsed some recent deals by pushing up shares of the acquirers. Innovation strategy has its rewards.

Avoiding Bubbles with Active Stock Selection

Can easy money chasing too many opportunities lead to market bubbles? It could. But is this 2000 all over again? Not necessarily for selective investors. Many dot-com stars with long-faded logos crashed and burned in 2000. But that era also begot lasting icons like Google and Amazon. Active investors who then focused on fundamentals, not fanfare, better discerned these and other eventual winners. We believe this holds true today, and the low cost of capital can make the strong even stronger and for a longer time. As long as they are fundamentally sound, even select high-priced technology stocks still have room to grow.

Overinvestment is another looming risk in a low-rate environment. Unfettered access to low-cost capital may incentivize some companies to heartily spend on misguided initiatives for all the wrong reasons. Cheap capital can spur unhealthy competition to invest more, but not always wisely. So active investors must carefully sift for the innovators destined to be future leaders.

Market pessimists believe low interest rates and aggressive fiscal policies have created too much money pursuing too many opportunities throughout the global system. But the value of future growth is almost always higher in a low-rate environment. This time, the climate is creating even richer breeding grounds for next-generation innovators—and for investors who can identify them early.

Related: The Pandemic Hits the Housing Market. What Can Advisors Do?

Lei Qiu is a Portfolio Manager on the International Technology Portfolio and a Senior Research Analyst for Thematic & Sustainable Equities at AllianceBernstein

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.