Written by: Bryce Coward | Knowledge Leaders Capital

Over the last few weeks there has been quite a bit of chatter among strategists about whether the market is undergoing a sustainable rotation into “value” stocks from “growth” stocks. It’s a bit surprising to us to see the outpouring of commentary on the issue, since by our work value has only outperformed growth by 3% or so since mid-July. Nevertheless, it is what it is, and so we thought we’d throw our hat into the ring on this issue.

When it comes down to it, there are a few key macro variables that are highly correlated with the relative performance of value vs growth – most of them measuring the reflationary impulse in the system in different ways. As reflation (or expectations thereof) plays out, it tends to be beneficial for the relative factor performance of value. This of course is due in part to the relatively higher degree of operating leverage among the value constituents. After all, a reflation that lifts all boats would tend to be highly accretive to the earnings of companies with relatively more levered income statements and balance sheets. The improvement in earnings subsequently actually reduces balance sheet leverage among value constituents to the extent that those earnings are retained, which provides a second-order reflexive dynamic as well.

As the reader can see in the table below, financial statement measures that are indirectly related to operating leverage like PP&E turnover and net debt are significantly different for value and growth companies. Value firms, having relatively higher levels of fixed assets, would stand to have a more pronounced improvement in PP&E turnover than growth firms in an across-the-board reflation. Value firms also have higher net debt levels than growth firms. As top lines improve in a reflation scenario, the debt servicing drag becomes relatively less for value vs growth firms.

So what are our market-based measures of the reflation dynamic saying currently? Are they telling us to get ready for a more durable move into value? The best we can say at this point is…maybe.

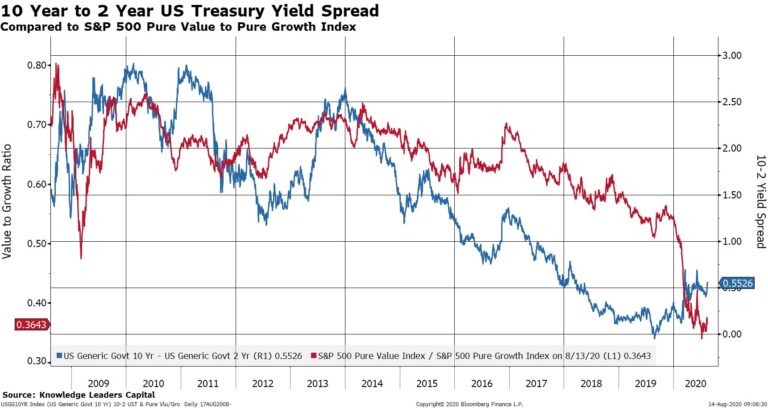

Let’s start with the yield curve. The 10-year minus 2-year Treasury yield spread is one of the best market-based reflation/disinflation measures out there since it factors directly into the profitability of bank lending, and therefore the velocity of money. To the extent that Treasury yields continue to have signaling value, the message coming from they yield curve is that there has been no mechanical change in the reflation dynamic since March. What we would need to see from the yield curve to signal a wholesale shift in value vs growth would be a pronounced widening of the 10-2 spread, which has yet to play out.

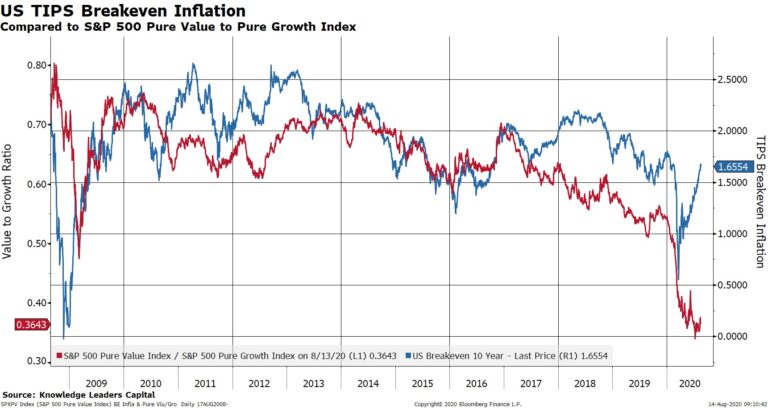

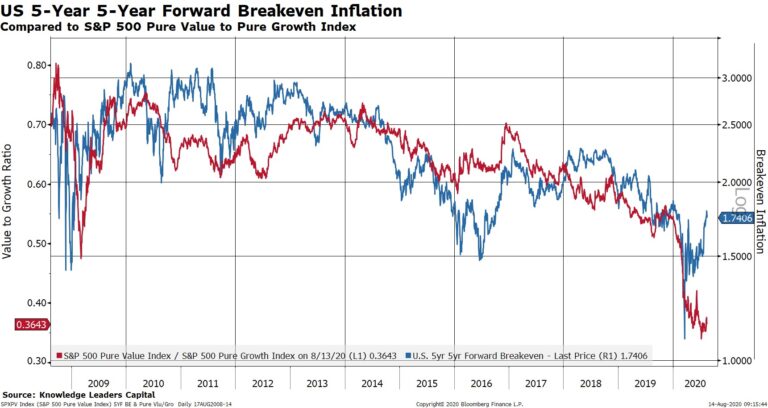

Next are inflation expectations. In charts 2 and 3 we should TIPS breakeven inflation expectations and 5-year 5-year forward expectations. The latter measures what 5-year inflation expectations are 5-years from now, which is a preferred indicator of the Fed. They are currently both sending a similar message, which is that market-based measures of inflation have moved up a lot since March, which should be supportive of value vs growth. But, we note that those inflation expectations remain anchored below average levels of the last cycle, which explains why value stocks have continued to underperform growth for most of the year. The recent experience suggests that we will need to see inflation expectations actually break above trend to get a more durable rotation into value.

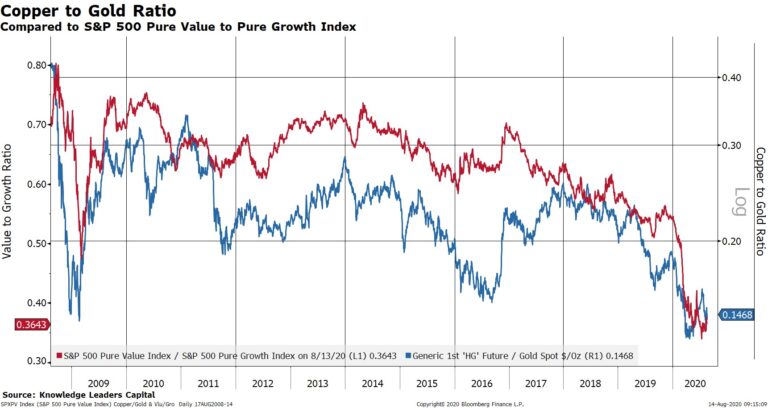

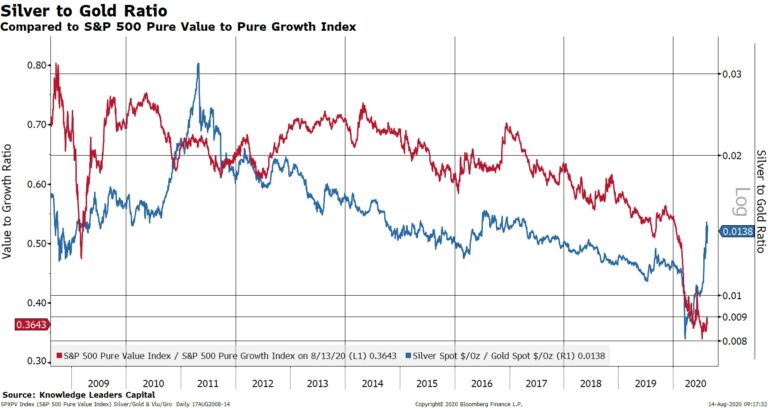

In the next two charts we highlight the how the relationship between industrial and precious metals informs, or at least reacts coincident to, the value/growth dynamic. Lasting reflations are typically associated with rising fixed capital formation and production, which requires rising usage of industrial metals such as copper or even silver. The metals with more industrial uses tend to outperform stores of value (gold) in reflation scenarios. The message we are getting from the metals space currently is mixed. Copper stopped underperforming gold earlier in 2020, but has made no real relative progress to speak of since then. Silver, on the other hand, has shown a more pronounced improvement vs gold.

Value stocks have outperformed growth stocks by a few percent since July, but at this stage we lack confirmation from market-based measures of reflation that the move is more than transitory. What we need to see more of is incentive for money growth (steeper yield curve), above trend inflation expectations, and confirmation from industrial metals that nominal growth is expanding. There is of course a policy mix that could usher in those things, like another round of fiscal and monetary expansion, but we are not there yet.

Related: Digital Advertising Industry and its Correlation to Economic Growth