The hedge fund industry is dynamic, comprising numerous strategies that attract varying degrees of interest over time. Demand for each strategy is impacted by many variables including capital market valuations, expectations of economic growth, market liquidity and risk appetite among others. Industry professionals spend a great deal of time analyzing these variables in order to identify which strategies they believe offer the best opportunities for outperformance. In this paper, we share some data and thoughts on where investors are focusing their time and resources starting with a brief overview of developments year to date.

2020 has been one of the most volatile years for the capital markets over the past century. The year began with questions looming about the sustainability of the seemingly ever-rising equity markets. That uncertainty accelerated dramatically at the end of the first quarter. Equity and credit markets experienced material market value declines in response to the expectation of a sharp economic stall instigated by COVID-19. Generally, most hedge fund strategies performed in line with investors’ expectations. Still, some less liquid fixed income strategies that were not properly hedged sustained large, unanticipated, drawdowns leading to large redemptions. In some cases managers imposed gates and suspended redemptions. A flight to quality by investors combined with a disproportionate amount of time required to address fund “blow ups” resulted in the postponement of the majority of new hedge fund allocations.

Entering the second quarter, the response of central banks around the world, in the form of massive monetary stimuli, drove nearly immediate, strong recoveries across the global capital markets. As a result, a large portion of world sovereign debt is trading close to 0% at mid-year. Concurrently, most equity markets are trading at valuations well above their historical averages, by the belief that monetary stimulus would result in a quick rebound in economic activity.

As the summer comes to a close, many of the drivers of volatility remain unchecked including the spread of Covid-19, the US trade war with China, the US election and massive increases in global debt. The big question is, how are investors processing these uncertain variables and what is the impact on their investment thinking?

One way to address this question is to ascertain which strategies are attracting current investor interest. As of last week, nearly 300 “approved” investors are registered to participate in the upcoming Gaining The Edge - Global Virtual Cap Intro event. In the registration process, they completed a detailed survey about what type of strategies and managers they are interested in meeting. Of the investors completing the survey:

- 33% are institutional investors(including large pensions, endowments, and foundations);

- 9% are advisors and OCIOs;

- 36% comprise family offices, multi-family offices, and high net worth individuals;

- 22% are funds of funds.

We believe this survey contains high quality data and provides an accurate depiction of current demand across the hedge fund industry. This is both a function of the composition of investors participating in these surveys and that these preferences will be shared with hedge fund managers as part of the meeting scheduling process.

From the survey data, we share the following observations:

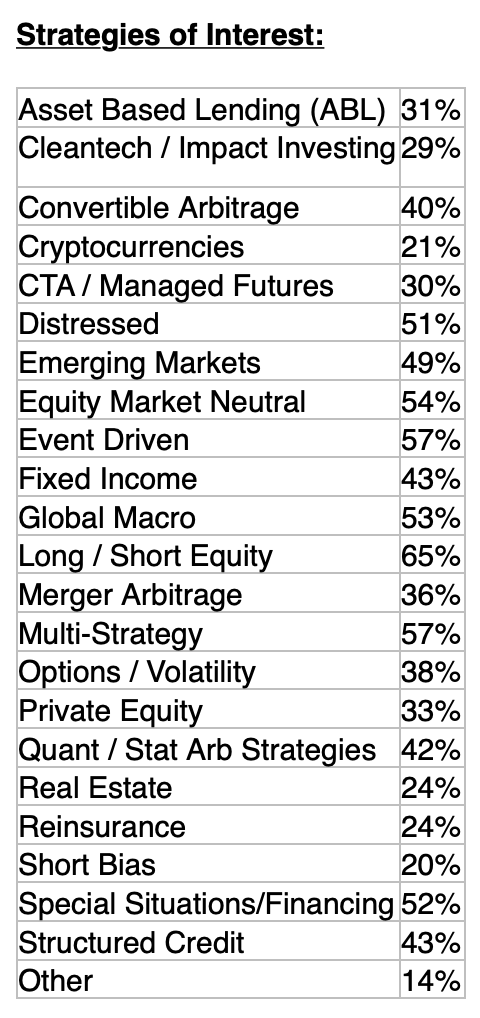

Investors were first asked to list their current strategies of interest. Long/short equity captured 65% of respondents, the largest share among all strategies. This indicates a positive change in investor sentiment regarding a fund manager’s ability to generate alpha in stock selection. Long/short equity has been losing market share for a number of years in the hedge fund industry and this data suggests a potential reversal of that trend.

Multi-strategy and event driven showed the second highest level of interest at (57%). This was followed closely by equity market neutral (54%), global macro (53%), special situations/specialty financing (52%), distressed (51%).

The increased interest in global macro, compared to a few years ago, indicates investor confidence that this strategy can take advantage of the increased volatility. More importantly this increase, along with the high level of interest in equity market neutral strategies, further supports the trend of increasing demand for strategies that are uncorrelated to the capital markets. Driving this trend are a combination of reducing portfolio tail risk and institutions shifting assets away from low yielding fixed income to a diversified portfolio of uncorrelated hedge fund strategies in order to enhance returns. Other strategies that will benefit from this trend include relative value fixed income, short term CTAs, and reinsurance.

The interest in distressed and special situations shows an increased willingness by investors to consider less liquid strategies along with a blurring of the lines between hedge funds and private equity as investors consider both structures to access these strategies.

A few niche strategies that are beginning to gain interest include cryptocurrencies at 21% and cleantech/Impact investing at 29%. Below is a full breakdown of the survey results.

In addition to indicating strategies of interest, investors were also asked to indicate the minimum fund size to which they would consider making an allocation. Of the respondents, 41% would consider new fund launches and an additional 23% were open to funds with less than $100 million. 32% of investors said they would consider funds between $100 million and $1 Billion and only 4% said they required a fund to be $1 billion or bigger. They were also asked about the minimum length of track record with 43% willing to invest with less than a one year record and 71% less than a 3 year record. These results were somewhat surprising, considering institutional investors represent almost one-third of those participating in the event (and this survey). However, this data confirms other indications that the minimum asset requirement for various investor types has declined over time and especially in the past several years. This may be, in part, attributable to the significant investment large pension funds have made into improving their internal processes. A majority have built out their research staffs and, in so doing, have increased their confidence and comfort with investing in smaller and emerging managers.

As we head into the 4th quarter, we anticipate an increase in hedge fund allocations due to pent up demand from earlier in the year. This survey should provide good guidance on the strategies to which assets will flow.

Additionally, as most investors and managers have become comfortable using Zoom and other virtual meeting providers, most will adopt this technology as part of their ongoing due diligence process. It will likely become a highly used tool to facilitate introductory meetings. In some cases, as we have already seen, investors may use virtual communication to facilitate their entire due diligence process.

Gaining the Edge - Global Virtual Cap Intro Event to benefit at risk youth is expected to be one of, if not the largest, virtual cap intro events in the industry. If you would like to see more information on the event please visit: https://www.agecroftpartners.com/virtual-cap-intro-2020

Related: How Do You Select a Long/Short Equity Hedge Fund Manager?