Written by: Brandon Buckingham, J.D., LL.M. | Prudential Financial

Get the facts on the unique features annuities provide for retirement planning

There is a lot of misunderstanding and misinformation about annuities. Yet for millions of Americans annuities serve an essential role in their retirement income strategy. The combination of investment and insurance features only available with an annuity, make it a critical component for investors looking to generate guaranteed income from their retirement portfolio. In addition, annuities offer tax deferral, a range of investment choices and legacy benefits.

Dispelling the Myths and Misconceptions

Annuities have had their share of detractors over the years. In fact, you may have seen disparaging advertising. But is such criticism warranted?

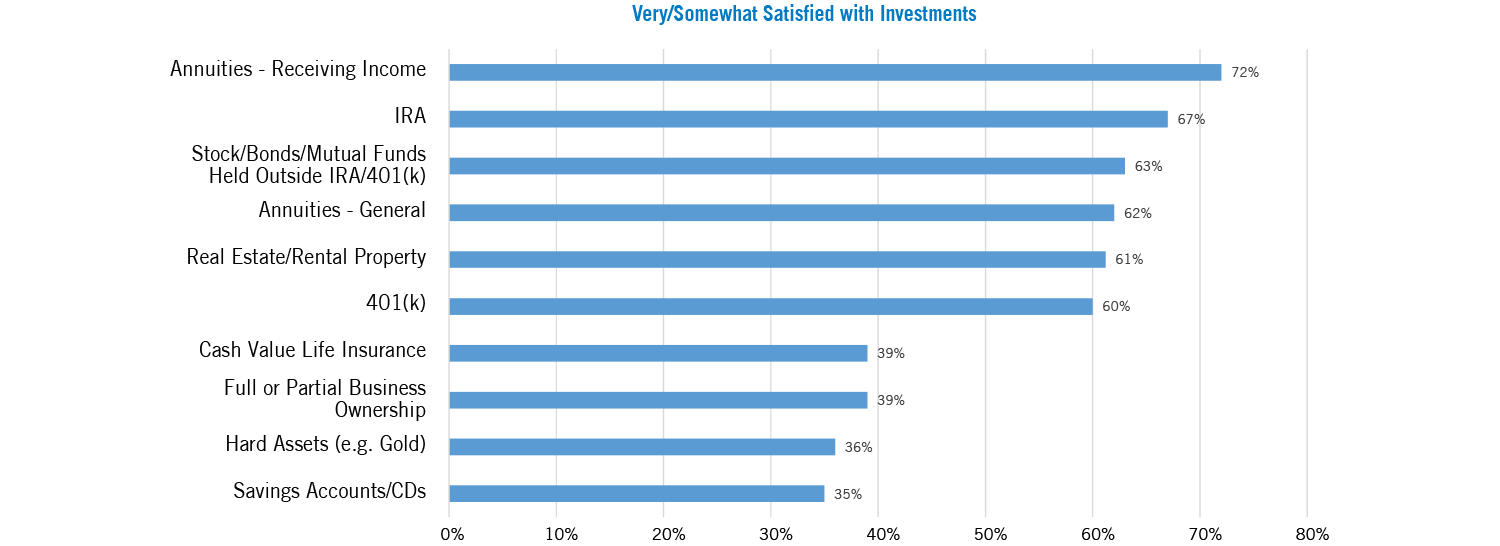

The reality is annuities currently serve a critical purpose within millions of Americans' retirement portfolios – adding a level of security, while helping alleviate some of the financial worry for the future. In fact, those receiving income from an annuity have the highest satisfaction levels of all investment types.1

While a strong retirement plan often requires a combination of strategies, investments and products, the best approach is to consider a client's objectives, goals and time horizon to determine if an annuity could make sense as a part of their overall plan.

Truth be told, no other vehicle combines the investment and insurance features to meet a wide range of client retirement needs.

Let’s take a closer look at some of those features:

Helping Clients Create Guaranteed Income for Life

While some say a guarantee may not be needed if investments perform well, the reality is that markets don’t just go up. Sometimes they go down, sometimes by a lot, and sometimes at the wrong time. Considering the current bull market is nearly 9 years old, this may be a good time to consider capturing market gains and continuing to invest with downside protection.

Annuities help retirees manage these critical retirement risks:

Longevity Risk

With people living longer, the challenge is to generate income that will last a lifetime. A 65-year-old married couple has nearly a 50% chance that one spouse will live to age 94, and a 25% chance to age 98.2 Investors should plan for a retirement that can last 25 years or more. With the decline of pensions and the future value of Social Security in question, annuities can help relieve a retiree’s fear of outliving their savings.

Market Risk

Longer lifespans mean the average retiree will likely face five bear markets in retirement.3 Since 1945 there have been 27 market corrections of greater than 10% and 12 bear markets with losses that exceeded 20% (two with a loss greater than 40% in just the last 20 years).4 Annuity guarantees can help retirees keep market downturns from derailing their retirement.

Sequence of Returns Risk

Losses in the early years of retirement can devastate a portfolio, increasing the likelihood that an investor will run out of money. Income guarantees can protect investors against the risk of retiring into a down market and help ensure their money lasts.

Investor Behavior Risk

Investors are often influenced by their emotions, causing them to get in and out of the market at the wrong time. This is evidenced by the fact that from 1997 through 2016, the S&P 500® Index gained an average of 7.68% while the average investor earned only 2.29%.5 The guarantees offered by annuities can give investors a level of confidence to remain invested through volatile markets.

Withdrawal Rate Risk

A safe and sustainable withdrawal rate is defined as how much can be taken from a portfolio with little probability of depleting the account. Historically that rate has been around 4%.6 However, because people are living longer in retirement and facing a prolonged low interest rate environment, new research suggests a sustainable withdrawal rate closer to 3% or less. An annuity’s guaranteed withdrawal rate is often higher, and can help mitigate this risk.

“Those receiving income from an annuity have the highest satisfaction levels of all investment types.”1

The Value of Guarantees

When planning, investors should always consider both the benefit and the cost when selecting any financial solution. Annuity fees are commensurate with the guarantees and features they offer. How much would you pay to insure your lifetime income? However, critics often compare investments based solely on expenses and ignore the unique value that annuities offer as a part of an overall strategy. Instead they should focus on whether the guarantees and other benefits offered by annuities, like added security, are worth the cost for a given investor’s situation.

Annuities Are Designed to Solve for Complex Client Needs

Annuities solve for more complex needs – such as providing guaranteed lifetime income; which cannot be outlived. Understanding an annuity and its guarantees is essential if an investor wants to make full and effective use of this type of investment.

Annuities Are Long-Term Investments

The perceived lack of liquidity is also something raised by annuity critics. But annuities are not for the short term. They are designed as long-term investments; after all, the purpose of an annuity is to generate income that will last a lifetime. Many annuity contracts have some form of “surrender charge.” This performs two functions. First, the surrender charge provides an incentive to hold the contract and ultimately reap the benefits it was designed to provide. Second, if an investor surrenders within a defined period after purchasing their contract, the company can recover its costs.

There are annuities without surrender charges, and “advisory” contracts where investors pay an annual asset-based fee, just as they do in managed money accounts. In addition, many annuity contracts have an annual free withdrawal privilege that allows owners to withdraw a certain amount of money without paying surrender charges.

Tax Benefits of Annuities

No one wants to pay the IRS more than they need to. Annuities provide an effective and efficient way to manage taxes. Critics argue that annuity distributions are taxed as ordinary income versus other investments which may be taxed at the lower long-term capital gains rate. But annuity investors generally take income over time in retirement. In these circumstances, the long-term benefits of tax deferral may offset the advantage of the lower capital gains rate. Alternatively, the buying, selling, and rebalancing within a taxable portfolio can result in additional taxes at the higher short-term capital gains rate. Comparatively, annuities provide tax-free rebalancing and the ability to defer taxes on any growth until income begins, often when investors are in a lower tax bracket.

Investors should also consider the tax benefits of asset location. It may be advantageous to have tax-inefficient assets such as actively managed funds, alternatives, REITs, high yield funds and taxable bond funds in tax-deferred accounts such as annuities.

Legacy Benefits of Annuities

Annuities may also provide owners the opportunity to grow, protect and control assets intended to pass to their loved ones. They are not subject to probate, avoiding associated expenses and delay. And annuities often provide various protective features such as enhanced death benefits, as well as flexible wealth transfer options. Another benefit is that beneficiaries may have the opportunity to “stretch” their inheritance, thereby spreading and deferring related taxes over their lifetime. Finally, they provide the owner the ability to control how and when the annuity benefits are distributed to their loved ones.

Annuities and other retirement accounts such as IRAs and 401(k) plans do not get a step-up in cost basis at death. “Step up” in cost basis generally benefits long-held individually owned stocks and real estate. A managed portfolio, on the other hand, will likely realize some taxable gains annually, adjusting the investment’s cost basis along the way, and reducing what may be available to be stepped up at death. Finally, it’s important to remember that most investors purchase annuities to generate guaranteed retirement income, so the lack of a step-up in cost basis may not be as important for that part of their portfolio.

The Foundation of a Comprehensive Retirement Income Strategy

While saving for retirement, an annuity’s underlying assets can be invested in subaccounts which own stocks and bonds. Having such market exposure can help create a hedge against inflation risk. But what about when the annuity’s income guarantee is turned on? Critics make the point that annuity income is not typically adjusted for inflation. Although this is generally true, it ignores what the annuity income allows the investor to do with their other investments.

Annuity income is the “floor” of a comprehensive retirement income portfolio, not the entire income plan. Many financial planners look at guaranteed income streams, such as those provided by pensions, Social Security and annuities, to help cover an investor’s essential retirement expenses – housing, food, clothing, transportation and healthcare costs. A strategy that ensures essential expenses are covered frees investors to devote more of their remaining capital to long-term growth. A comprehensive retirement income plan should include both sources of guaranteed income and non-guaranteed investments.

Investor Satisfaction

As previously mentioned, the fact is that consumers who own annuities and are receiving income are more satisfied with their annuity than any other investment.

Conclusion

While planning for retirement, a fully informed investor is in a better position to make the right decisions regarding their needs, goals and objectives. No one product or investment will make a comprehensive financial and retirement plan successful; it often requires a combination of various strategies, investments and products. Work with your clients to thoughtfully consider whether the guarantees, tax, legacy or planning benefits of an annuity are right for their overall financial plan.