First it was the U.S. Federal Reserve. Then, in 2013, Japan launched what became known as Abenomics. The European Central Bank (ECB) followed suit in 2014. And now the People’s Bank of China has joined the parade.

All of them in some way stimulated economic growth by initiating monetary quantitative easing (QE) programs.

The media and politicians applauded them for their QE plans. All of them, that is, except for China. Instead, we’ve only seen a flurry of negative headlines.

I often tell investors to follow the money, which currently is cheap to borrow. Cheap money is good for stock prices, but not for retired folks who have most of their savings in term deposits with low interest yields.

Most important for commodity investors is the powerful correlation between China’s money supply and commodity prices. The money supply peaked in 2011 and has been falling along with commodity prices.

On Monday, China unexpectedly trimmed the value of its currency, the renminbi, 2 percent, the most in two decades. In the days since, many analysts and “experts” have irrationally turned sour on the Asian country, similar to the extreme bearishness toward gold in the last month.

But investors last week came home to the yellow metal after China announced it had increased its gold reserves by an additional 19 tonnes in July, boosting its total holdings to 1,677 tonnes (nearly 54 million ounces). This helped prices rally 1.4 percent on Wednesday to reach $1,124.46, a three-week high.

Investors should likewise return to China when they realize that the global reaction to the renminbi devaluation has been hugely overblown. I agree entirely with my friend Addison Wiggins, who writes in his Daily Reckoning newsletter:

The market is up in arms about this currency move. And frankly most things that I read from the market have it all wrong…

They make China out to be the big, bad villain—calling this move manipulation or a “currency war.” And while EVERYTHING that central banks do is indeed manipulation or a “currency war”—why don’t we hear those terms thrown around the ECB or the U.S. Fed?

To help cut through the noise and get a more balanced picture of devaluation's causes, effects and possible ramifications, I chatted with our resident Asia expert Xian Liang, portfolio manager of our China Region Fund (USCOX) . Below are some of the highlights.

As you know, we follow currencies very closely in our investment team meetings because we’re aware that government policy is a precursor to change. Having said that, why did China decide to devalue the renminbi?

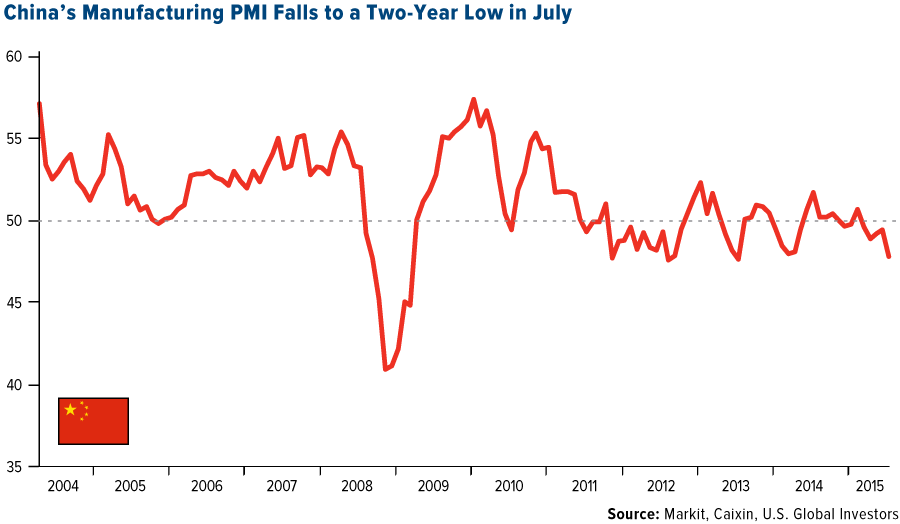

There are several possible reasons, the first one being economics—specifically, to stimulate economic growth and ease liquidity in the financial sector. A weaker renminbi can help make Chinese exports cheaper for foreigners and imports dearer for locals, creating the incentive for a “net inflow” of money. July data shows that economic activity remains worse than expected. China’s purchasing managers’ index (PMI) reading for the month is one example, but fixed-asset investments, power generation and exports were all down.

Deflationary pressure also intensified in July, and the renminbi in trade-weighted terms—that is, against a whole basket of major trading partners’ currencies, not just the dollar—has soared to record highs. This is because of a de facto peg to the dollar, making Chinese goods and services uncompetitively priced to world customers.

Another reason is domestic politics. Chinese policymakers want to resurrect their reformist image among domestic intellectuals and the middle class by yielding more power to market forces to determine its currency exchange rate, which offers some compensation for July’s aggressive, command-and-control intervention in the A-Share market.

And then there’s international politics. It’s well known that China wishes its currency to be included in the International Monetary Fund’s special drawing rights basket, along with the U.S. dollar, euro, British pound and Japanese yen. Chinese policymakers are actively demonstrating to the IMF their commitment to “a more market-determined exchange rate,” a critical step toward eventual renminbi internationalization.

Many countries have devalued their currencies lately—Japan, Germany, France and others. Business Insider, in fact, just shared a Goldman Sachs chart showing how miniscule the renminbi’s depreciation really is compared to other emerging countries’ currencies. And yet China gets singled out in the media! Why is everyone so hard on China?

What’s usually not mentioned in all the news and editorials we’ve seen is that China hasn’t resorted to currency devaluation in 20 years. For the last decade, the renminbi was largely moving in a single direction—up—because China was tired of being dubbed a currency manipulator and it would like to foster consumerism.

As the second-largest economy in the world, China is interested in transforming its growth model from investment-driven to consumer-driven, and some investors might wonder how the devaluation will affect consumption. Today, the richer Chinese middle class is made up of big spenders, both home and abroad, and a weaker renminbi translates to weaker purchasing power for them. It might also have larger implications for global tourism, global consumer goods and global property. So the difference between China and, say, France is pretty significant.

A lot of people think the Federal Reserve will hike interest rates this year—maybe even as early as September—though I’ve expressed doubts about that. Will the devaluation have any effect on the Fed’s decision?

To the extent that it weakens its own currency, China exports deflation to the U.S. and can help the dollar’s strength. Lower inflation and a stronger dollar reduce the incentive or rationale for any imminent Fed rate hike. So yes, you can almost say this is China’s silent protest against the widely anticipated September hike. China seems to be reminding Janet Yellen that in today’s interconnected world, unilateral monetary policy action by the U.S. without first considering global dynamics might not be the smartest thing to do. In effect, it’s saying: “Here’s a preview of what could happen if you insist on hiking rates this year.”

Is this a sign of further reforms? What else can we expect?

The devaluation does indeed herald back to the days of major Chinese reform. In fact, it occurred one day after China approved a comprehensive plan to reform its state-owned enterprises to make them more market-driven, similar to those in Singapore. So at least the government welcomes the perception that the devaluation has more to do with long-term structural reform and less to do with short-term expediency.

Investors are being bombarded with bad news about China right now. There have been some very negative headlines. Where’s the good news in all this?

Here’s the simple answer: A weaker currency not only helps Chinese exporters but also U.S. consumers. Whether you buy things made in China or are planning your next vacation there, you’ve got money to save now. Opportunities have also been expanded for U.S. retailers and manufacturers that source from China, not to mention U.S. airlines. And if you’re in the camp that believes this devaluation is the start of a new “currency war,” then it might be time for gold to shine.