Written by: Samantha Azzarello and Corey Hill

A top client question has been about new market highs. In particular, where do we go from here when allocating to equities? This question is deserving of commentary and analysis from the powerful vantage of where portfolios are currently positioned.

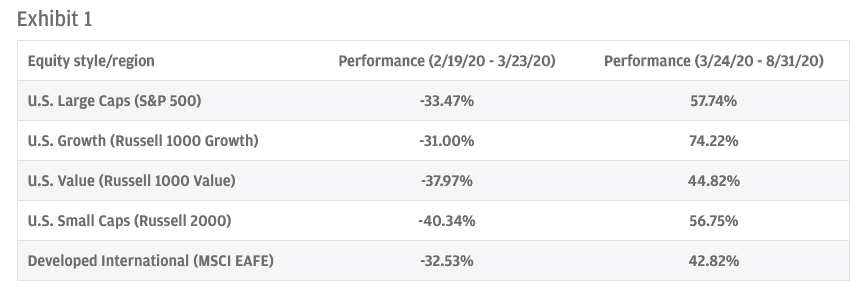

As the economy & markets continued to grind higher, investors entered into 2020 with prominent portfolio overweight’s into U.S. and Growth oriented equities. Then came February 19th. Over the course of just over a month, the S&P 500 closed down over 33%. While no one style or region was spared, Large Cap tended to outperform Small Cap, and a similar story resulted for Growth vs. Value. Developed International also experienced similar pain to U.S. markets (Exhibit 1). Our Portfolio Insights program experienced a significant increase in usage during that timeframe but the swift and violent nature of this drawdown resulted in most portfolio positioning remaining unchanged.

As fiscal spending and fed policy left no stone unturned to aid the ailing global economy, the S&P 500 has since rallied nearly 58% as of August 31st. While this rally has generally offset the Q1 market pullback, how it went about doing so was starkly different. The areas of the market that have been dominant over recent years continued this trend and to some extent exacerbated the dispersion even further. The best example of this is the outperformance of U.S. Growth, delivering ~30% better returns than U.S. Value. And while Developed International equities moved directionally with domestic, its recovery did significantly lag in a relative sense (Exhibit 1). With the attribution of the Q1 pullback being so broad and Q2 recovery being so concentrated, it’s prudent to revisit where we started entering into 2020.

As we consider the lean toward U.S. and Growth stocks entering into the year, we must acknowledge the disparity in the Q2 rally. Many of the portfolio biases exhibited entering 2020 are attributed to the Q2 rally. As most portfolios remained relatively unchanged at market lows, those same biases have become even more pronounced. For instance, the current average moderate portfolio we analyze contains nearly double the exposure to Growth relative to Value.

If one had started the year at a 50-50 split between Growth and Value, the significant dispersion in performance has led to meaningful skew. If left unchanged throughout the ups and downs of 2020, the current allocation would be in the realm of 59% Growth & 41% Value.

While this year has provided us with some of the more turbulent markets on record, we should continue focusing on building well diversified all weather portfolios for the long-term. Now poses an excellent time to consider rebalancing your allocations back to neutral or a portfolio check-up to understand if additional opportunities exist with regard to overall positioning and/or investment selection.

With the fastest recovery on record, it’s important to not let emotions or behavioral biases, like loss aversion (holding on to large cash allocations) or recency bias (expecting more of the same trend from market and investment performance), take hold. Instead, making decisions based on data and analysis is the best course of action. Whether it be rebalancing to a desired asset allocation or finding implicit over and underweights, reviewing your portfolio and underlying investment performance makes sense.

Feel free to leverage our Portfolio Insights tools and consult with one of our Portfolio Specialists to confirm positioning and ensure your investments are serving their intended role in your portfolio.

Related: How Would a Corporate Tax Hike Impact the Recovery?