Written by: Monica Kingsley

Right after the open, stocks took again on the 61.8% Fibonacci retracement, but retreated. Trading around the 2910 mark in a tight range, it appeared as base-building for the decisive push above the resistance. Instead, stocks fell through in the final hour of trading, coinciding with the Fed’s Kaplan and Kashkari tweets. Have they been a game changer?

S&P 500 in the Short-Run

Let’s start with the daily chart perspective (charts courtesy of http://stockcharts.com):

Opening again almost at the 61.8% Fibonacci retracement, the bulls’ attempt to move higher fizzled out. Stocks declined, but not profoundly. That came only with the latest Fed pronouncements. This is how we commented on them in our intraday Stock Trading Alert earlier today at 2:30 AM EST:

(…) The slide in stocks later yesterday may look to be a decisive start of a downtrend, but it lacked volume rising well above previous sessions. Then, let’s consider the context. What groundbreaking message did Fed’s Kaplan or Kashkari say? That more fiscal stimulus might be necessary, and that we need to get the virus under control so as to fix the economy. Well, both statements are more than kind of obvious.

Finally, the overnight price action is bullish – after the initial hit, we got another downswing attempt refused, and fast. The same goes for the one-hour old attempt to reverse the upswing from the overnight bottom.

Since then, the bears pushed the futures once again to 2850, but after stabilization, prices rebounded to 2870. As a result, the above observations still remain valid.

Notably, we’ll get the Fed Chair Powell to speak and take questions at the Peterson Institute for International Economics webinar – at the US market open. The timing is peculiar to say the least, bringing back the memories of April 09, which is when the $2.3T backstop bombshell was dropped, powering stocks higher in its aftermath.

While past events are no guarantee of the future, the similarities are there. Another surprise statement wouldn’t surprise us, as the Fed hasn’t been projecting the aura of strength and decisiveness for a few weeks now. Considering the pace of events, that’s quite a long time these days. And yesterday’s price action appears to be a call to do something, as in twisting the Fed’s hand. Has it been enough?

Will the Fed banish the shadow of the doubts that lingers over the markets in recent weeks? Will fiscal policy ride to the rescue too? As we’ve seen yesterday both in stocks and bonds, the markets are calling for that. And we don’t expect the Fed to throw up their hands and say they gave it their best shot…

The Credit Markets’ Point of View

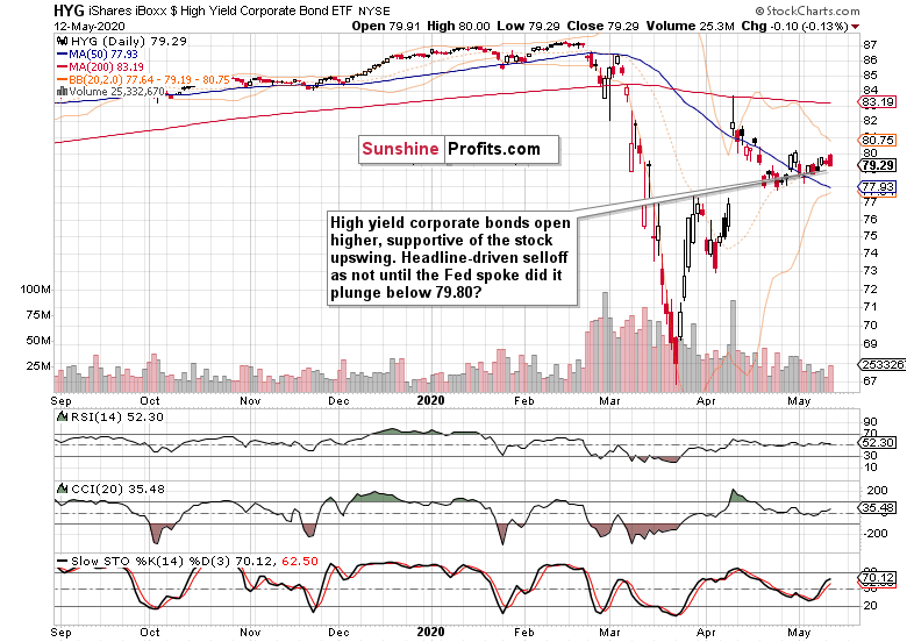

Opening with a bullish gap, high yield corporate debt (HYG ETF) modestly retreated in tandem with stocks. The sizable red candle was again born in the final hour of trading. Remember that the Fed’s vehicles to enter the debt ETF markets are ready now, and each successful debt rollover would support stocks. It makes a world of difference, having to pay just the coupon or the principal.

Such interventions work to push both stocks and bonds higher, at the cost of zombification of the economy (who in their right mind would backstop airline or cruise companies’ debt on currently prevailing terms?) and misallocation of capital. But that’s a story for another day.

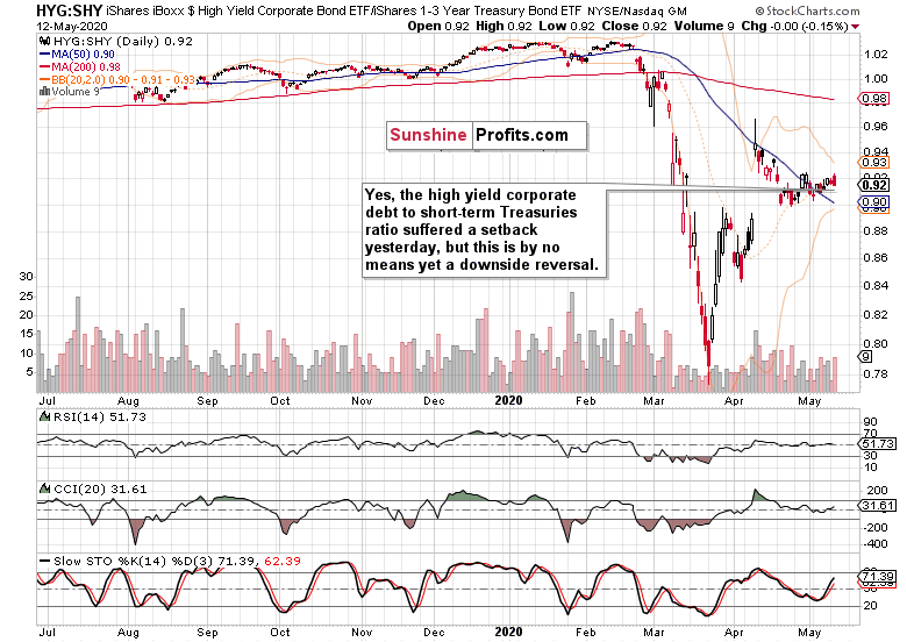

Importantly, the junk bond ratio to short-dated Treasuries (HYG:SHY) confirms the above assessment. We have seen no downside reversal as both the ratio and the HYG ETF are trading solidly above the late April lows. As a result, the most likely resolution of this consolidation is to the upside.

Key S&P 500 Sectors in Focus

Understandably, both the heavyweight and early bull market sectors took a beating yesterday. The Russell 2000 (IWM ETF) also declined, and on higher relative volume than the S&P 500 did. While that’s bearish, the credit markets don’t support jumping to conclusions just yet. In other words, the bear market can’t be yet declared to have resumed just because reaching a 50% or 61.8% Fibonacci retracement after a historic selloff is a hallmark of bear market rallies.

Yes, that’s true despite the sizable reversal on meaningful volume in both technology (XLK ETF) and healthcare (XLV ETF), or the continuing underperformance of financials (XLF ETF).

Neither energy, nor materials slash industrials had a good day yesterday. While the early bull market trio seems to be running into headwinds, they have not rolled over decisively.

Summary

Summing up, despite the stock bulls being again rejected at the 61.8% Fibonacci retracement, the bullish case isn’t yet lost. How close to being over is the deterioration in the stock upswing internals? Credit markets hint at a temporary setback only. Our open long position remains justified, and needs to be tightly managed.

Related: Are Rallying Stock Markets out of Step With Economic Reality?